The Broke Student’s Guide to Zero-Stress Budgeting (Using the 50/30/20 Rule)

VR Team

VR Team- December 28, 2025

It’s 11:00 AM on a Tuesday. You’re running on three hours of sleep and an iced coffee that cost way too much. You check your banking app before buying lunch, and your stomach drops.

Sound familiar?

The “broke college student” trope is funny in movies, but in reality, it’s stressful. Between tuition, textbooks that cost as much as a car payment, and trying to have an actual social life, managing money in college feels impossible.

Here is the truth: You don’t need more money to stop feeling broke. You need a better system.

Forget complicated spreadsheets. This student budget guide is for students who want to handle their money without making it a second major.

Real Talk: It is okay if your income changes every month. You need a budget flexible enough to handle the chaos of semester life, not one that makes you feel guilty for buying a textbook.

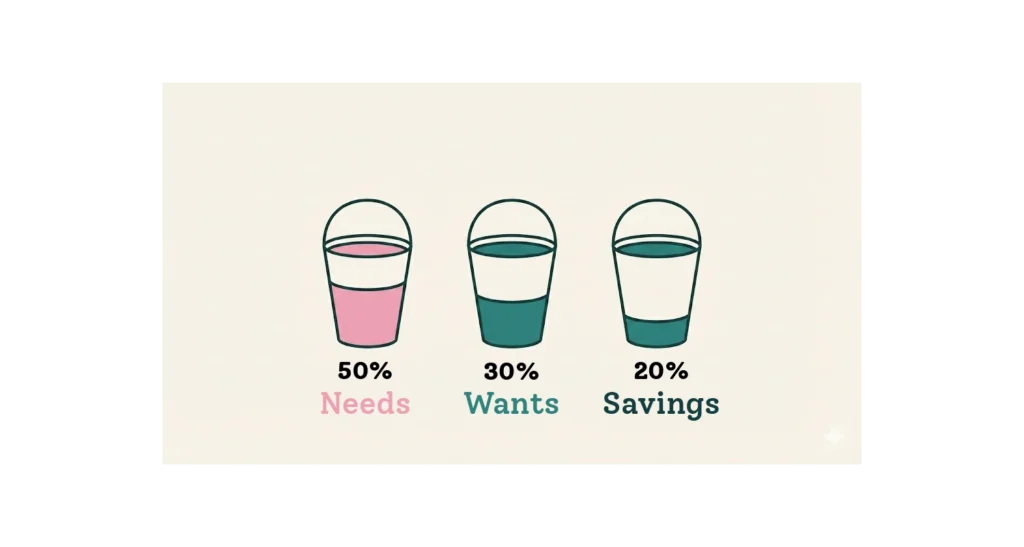

The Core of Your Student Budget Guide: The 50/30/20 Rule

1. The “Survival” Bucket (50% – Needs)

These are the non-negotiables that keep you enrolled and housed.

- Rent/Dorm fees

- Groceries/Meal plan

- Tuition payments

- Phone bill/Utilities

2. The “Sanity” Bucket (30% – Wants)

Do not skip this. College is miserable if you can’t ever say “yes” to plans. This bucket is for Friday night pizza, streaming services, concert tickets, and yes—your morning coffee. As long as it fits in this 30%, spend it guilt-free.

3. The “Future You” Bucket (20% – Savings/Debt)

This is the hardest part, but the most important.

- Emergency Fund: Even $20 a month adds up for when your laptop inevitably crashes.

- Debt Prep: If you have loans, try putting a tiny bit aside now to lower the interest later.

Student Budget Guide Examples: Real Scenarios

Scenario A: The "Lump Sum" Student (Financial Aid)

If you survive on student loans or a scholarship, check that drops once a semester, you have the “Feast or Famine” problem. You feel rich in September ($5,000 in the bank!) and destitute by December.

- The Fix: The “Pay Yourself” Method.

- Take your total semester income (e.g., $4,000).

- Divide it by the number of months in the semester (4 months).

- Result: You have a “salary” of $1,000/month.

- Action Step: Keep the big chunk in a savings account and set up an automatic transfer of $1,000 to your checking account on the 1st of every month. Pretend the rest of the money doesn’t exist.

Scenario B: The Server / Gig Worker (Variable Income)

If you drive for Uber Eats or wait tables, your income is unpredictable. One Friday you make $300; the next, you make $50.

- The Fix: The “Lowball” Average.

- Look at your lowest income month from the past year. Let’s say it was $800.

- Build your “Needs” (50%) bucket based on that $800 worst-case scenario.

- Any extra money you make on a good week goes straight into your Savings or “Fun” bucket. This way, your bills are always paid, even on a slow month.

3 Money Leaks You Need to Plug ASAP

Before you set up your budget, stop bleeding cash in these three common student traps:

The Textbook Scam

The "Little Treat" Trap

A $6 coffee every day is $180 a month. That’s a utility bill. We aren’t saying cut coffee entirely (see the 30% “Wants” bucket), but maybe buy a nice travel mug and make it at home four days a week.

Subscription Creep

Do you really need Netflix, Hulu, Disney+, HBO, and Spotify Premium? Rotate your subscriptions. Pay for one month of Netflix, binge everything, cancel it, and switch to Hulu the next month.

The Battle of the Budget Tools: What Should You Use?

- The “Bullet Journal” Method (Pen & Paper)

- Pros: Extremely aesthetic and satisfying to draw. Great for “Velvetrows” vibes.

- Cons: Zero automation. You have to do the math yourself. If you make a mistake, you have to use white-out.

- The “Fancy App”

- Pros: Connects to your bank account automatically.

- Cons: Often costs a monthly subscription fee (ironic when you’re trying to save).

- The Automated Spreadsheet

- Pros: The perfect middle ground. You get the control of a notebook with the “math brain” of an app. You pay once (no subscriptions) and own it forever.

- Cons: You have to enter your spending manually (which actually helps you spend less because you “feel” the purchase).

Stop Doing Math in Your Head (Automate It)

You have enough homework. Don’t make budgeting another assignment.

The hardest part of the 50/30/20 rule for students is calculating the percentages every time you get paid, especially if your paychecks vary.

We built a tool specifically to handle this. You just type in your income, and it automatically tells you exactly how much you can spend on “Wants” this month without going broke. It even handles biweekly paychecks perfectly.

Frequently Asked Questions (FAQ)

Does this student budget guide work for international students? Yes. The principles in this student budget guide work with any currency, whether you use Dollars, Euros, or Dirhams.

Why is this student budget guide different? Most advice assumes you have a salary. This student budget guide is built specifically for irregular income and financial aid drops.

“How do I save money on things I actually need?” The most underused asset you have is your Student ID.

- The Rule: Never pay full price without asking. From music streaming services to clothing stores and movie theaters, your student status often gets you 10-50% off.

- Action: Before you tap your card, always ask: “Do you offer a student discount?”

“How much should be in my Emergency Fund?” Standard advice says “3 to 6 months of expenses,” which is laughable for a student.

- Start with a Micro-Goal: Aim for $500. This is enough to cover a laptop repair, a lost phone, or an urgent travel ticket home. Once you hit that safety net, you will sleep much better.

“How do I say ‘No’ to friends without looking broke?” FOMO (Fear Of Missing Out) is real. Instead of saying “I can’t afford it,” try suggesting an alternative:

- Expensive: “Dinner and drinks downtown?”

- Alternative: “I’m saving up for a trip. Want to grab a coffee and walk around the park instead?”

- Real friends won’t care how much you spend; they just want to hang out.

Final Thought

College is supposed to be an amazing experience. Don’t let financial stress ruin it. Get a simple plan in place now so you can focus on what matters—passing those exams (and having fun doing it).