Zero-Based Budgeting vs. 50/30/20

VR Team

VR Team- December 27, 2025

It’s Sunday night. You sit down with a pile of receipts, determined to track every single latte you bought this week. You open a blank spreadsheet, ready to take control.

By Tuesday, you’ve missed an entry. By Friday, you’re too scared to check your bank account, so you give up entirely.

If this sounds familiar, I have good news: The problem isn’t you. It’s that most traditional budgeting methods aren’t built for your brain.

Most financial advice is written for accountants, not humans. Today, we’re going to look at the battle of Zero-Based Budgeting vs. 50/30/20 to find a method that allows you to buy the latte and pay your rent.

The Psychology: Why Most Budgeting Methods Fail

The reason you have failed at budgeting before isn’t because you are bad at math. It is because you picked the wrong system for your personality type.

In the world of budgeting methods, self-awareness is more important than discipline.

The Zero-Based Budget requires high “Conscientiousness.” It is for the person who loves control, details, and checking boxes. If you color-code your calendar, this is for you.

The 50/30/20 Rule requires “Big Picture” thinking. It is for the person who wants safety but hates micromanagement. If you just want to know you aren’t going broke without tracking every coffee, this is your match.

Choosing between these budgeting methods is like choosing between Android (customizable) and iPhone (simple). Neither is wrong, but using the one that doesn’t fit your brain will drive you crazy.

Why Zero-Based Budgeting Feels Like a Second Job ?

If you’ve searched for “how to budget,” you’ve probably seen the Zero-Based Budget.

The concept is simple: Every dollar has a job. If you earn $2,000, you must assign every single penny to a category until you have $0 left.

$800 for Rent.

$200 for Groceries.

$4.50 for Coffee.

The Problem: While this offers total control, it requires constant maintenance. If you overspend by $5 on snacks, you have to move $5 from somewhere else. For students, freelancers, or anyone with a busy life, this level of micromanagement is exhausting.

Real Talk: Budgeting shouldn’t feel like punishment. If your system requires you to feel guilty about a $5 purchase, it’s not sustainable. You need a plan that bends so it doesn’t break.

The 50/30/20 Rule (Financial Clarity)

Enter the 50/30/20 Rule. This method was popularized by Senator Elizabeth Warren, and it is the “Holy Grail” for anyone searching for a simple budget template.

Instead of tracking every penny, you just split your income into three buckets:

- Needs (50%)

These are your survival costs: Rent, utilities, groceries, and minimum debt payments. These are non-negotiable.

- Wants (30%)

This is the fun part. Dining out, Netflix, hobbies, and yes—your morning coffee.

- The Secret: This isn’t “wasteful” spending; it is Guilt-Free Spending. As long as you stay within this 30% bucket, you never have to question a purchase again.

- Savings (20%)

This is for “Future You.” It covers your emergency fund, investments, or saving up for that dream vacation.

| Feature | Zero-Based (Control Freaks) |

50/30/20 (Students & Beginners) |

|---|---|---|

| Best For... | Debt Control | Peace of Mind |

| Time Required | High (Daily) | Low (Weekly) |

| Flexibility | Rigid | Fluid & Easy |

| Psychology | Restriction | Balance |

If you are a student or just starting out, the 50/30/20 rule is often the better choice because it allows you to live your life without constantly checking a spreadsheet.

The "Hidden" Problem: The Biweekly Paycheck

There is one snag that trips up almost everyone. Most budgeting advice assumes you get paid once a month.

But if you get paid biweekly (every two weeks), the math gets messy.

Most months you get 2 paychecks.

Two months a year, you get 3 paychecks.

If you try to divide your monthly rent by two paychecks manually, you might end up short on cash at the end of the month. You need a system that automatically calculates the “26 Paycheck Year.”

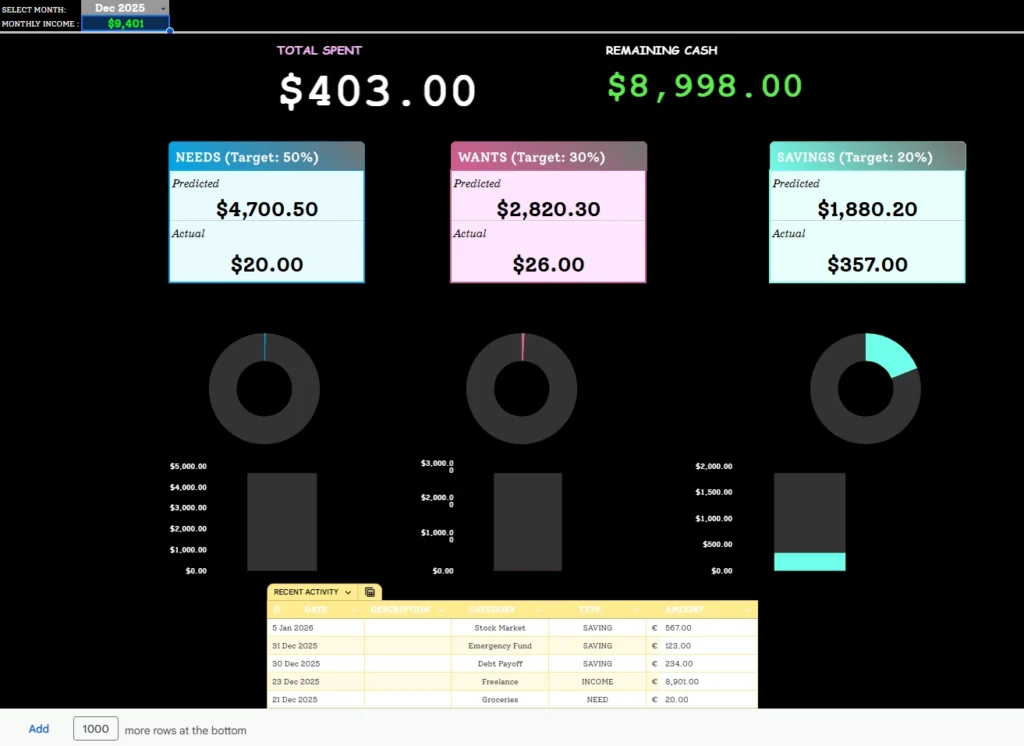

Automate the Boring Stuff

You could sit down with a calculator every other Friday and try to split your paycheck into 50/30/20 buckets manually… OR you could let a template do it for you.

We designed the 50/30/20 Budget Planner specifically to solve the math anxiety.

Biweekly Calculator Built-In: Just enter your paycheck amount, and it instantly tells you exactly how much is safe to spend.

Visual Dashboard: See your “Guilt-Free” money in clear, aesthetic charts.

No “Excel” Skills Needed: It’s a simple Google Sheet that does the heavy lifting for you.

The "Hybrid" Approach (The Velvetrows Method)

Can’t decide? You don’t have to. The secret third option among budgeting methods is the Hybrid Model.

Many of our users at Velvetrows start with the structure of the 50/30/20 rule but use a Zero-Based tracker for just their “Wants” category.

Automate the Needs: Your rent and bills are fixed. You don’t need to track them daily.

Track the Fun: Use a Zero-Based sheet to track your 30% “Wants” money. This gives you the guilt-free spending of the 50/30/20 rule but the awareness of Zero-Based budgeting.

This is often the most sustainable of all budgeting methods because it balances automation with awareness.

Final Thoughts

The best budget isn’t the most complicated one. It’s the one you actually stick to. Stop trying to be perfect with your money, and start trying to be consistent. Your future self (and your savings account) will thank you.

FAQ: Budgeting Methods Explained

Which of these budgeting methods is better for debt? The Zero-Based Budget is superior for debt payoff. Because you assign every dollar a job, you can aggressively target debt. The 50/30/20 rule is often too passive for rapid debt elimination.

Are there other budgeting methods I should know? Yes, there is the “Envelope System” (cash only) and “Pay Yourself First” (savings focused). However, in the digital age, Zero-Based and 50/30/20 remain the two gold standards for spreadsheet users.